Gazprom: more than ever a long-term buy?

27 March 2020

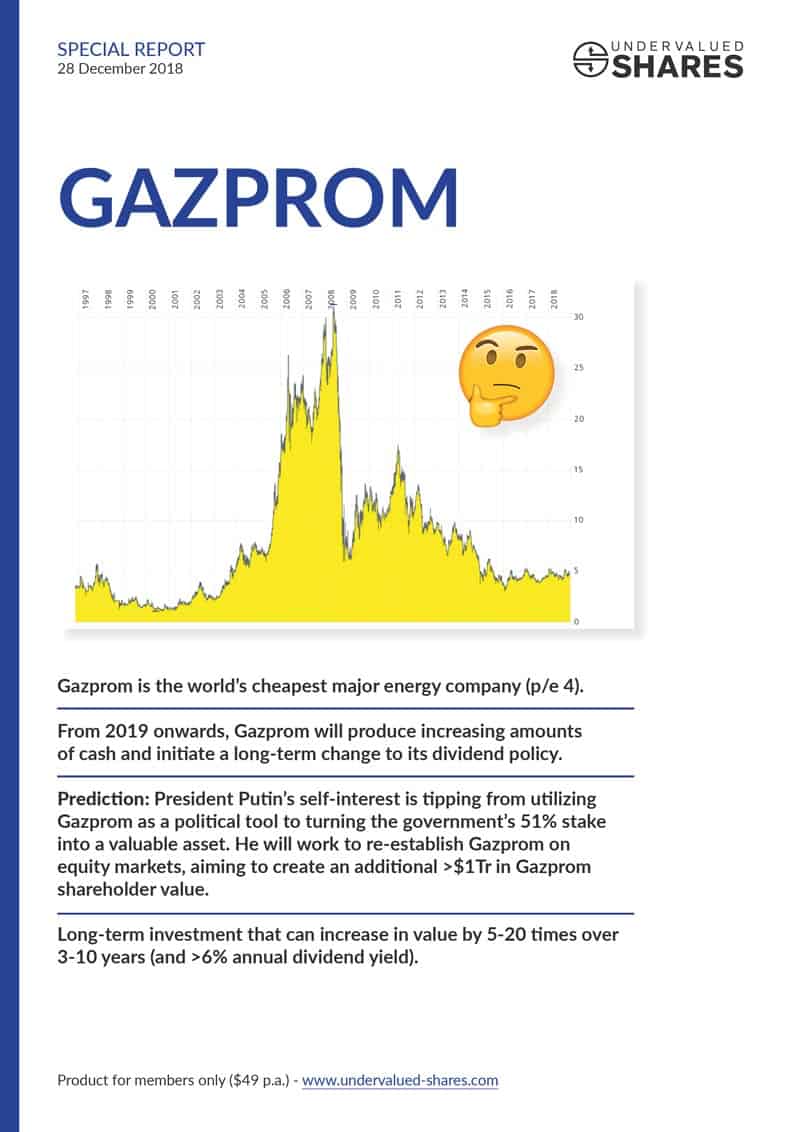

The stock of Gazprom rose 128% after my December 2018 report, but has since lost most of its gains due to the double-whammy of the coronavirus crisis and oil price crash.

Is now a second opportunity to get onboard at fire-sale prices?

This report provides you with a very different perspective to the one shared by conventional investment media. It spells out the "10 reasons to be invested in Gazprom for the next 10 years".

Short term, the company probably offers a double-digit (!) dividend yield.

Long term, it's one of the most compelling corporate restructuring stories you can find on the world's stock exchanges. If Putin plays his cards right (as he has done recently), Gazprom shareholders could earn hundreds of billions of dollars between now and 2030. If you missed the FAANG stocks in the 2010s, you might want to consider owning Gazprom for the 2020s.

This report is both an update to my December 2018 report and a standalone piece that you can read without prior knowledge of the company.